Home > Life stages >

Hello pension, goodbye tension

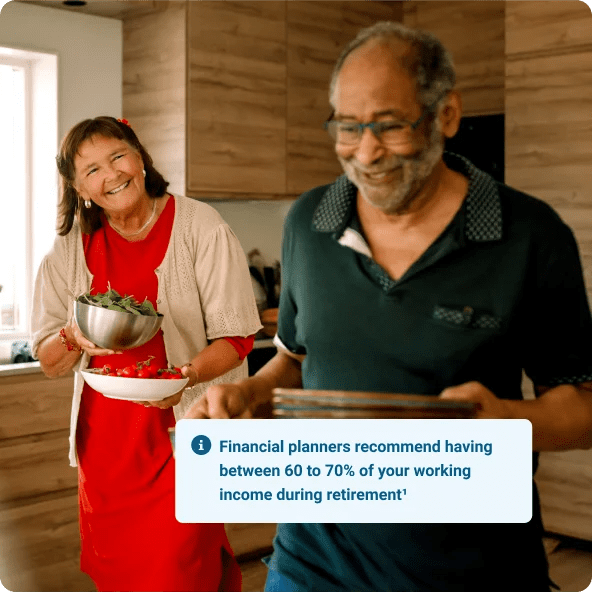

You’ve earned your retirement. But your nest egg may not fully cover your healthcare or unexpected costs — and that’s where insurance comes in.

How insurance keeps you covered during retirement

In retirement, your income may be predictable — but life isn’t. Get ahead of illness, unexpected fees and and financial instability with an insurance plan built for your lifestyle.

Three ways to create stability in retirement

From ensuring reliable income to preparing for rising health needs, these are the core protections that help retirees enjoy peace of mind in their next chapter.

-

Keep your loved ones and estate ready Make it easy to cover taxes, debts, and final expenses so your plans stay intact.

-

Protect retirement from a serious health event A diagnosis should not derail your income plan or force difficult tradeoffs.

-

Turn savings into reliable income and protect what you keep Convert savings into regular income with options to help protect your investments.

RBC Growth insurance (participating whole life)

Lifetime protection that also builds cash value. If you’re looking for a policy that’s guaranteed to grow and is designed to offer permanent lifetime protection this is it.

Highlights

Coverage of $25,000 to $25,000,000 for life.

Available to purchase at ages 0-85.

Dividend Options – choose from five flexible options for receiving dividends (Paid-up Additions, Cash, Premium Reduction, Enhanced Insurance or Dividends on Deposit).

World-Class Asset Management with an RBC investment team.

Single or Joint Coverage.

Access to your accumulated cash value at any time.

RBC Universal life insurance

Get long-term protection with this flexible solution offering lifetime coverage and tax-deferred investment growth.

Highlights

Coverage from $50,000 to $25,000,000 for life.

Choose how much to pay into your policy and how you want to pay your premiums.

Create the portfolio that is right for you with a range of investment options.

Available for Canadian residents aged 0 to 85 years old.

RBC critical illness insurance

Protect yourself financially against the most common illnesses. Together, cancer, heart attack and stroke make up 89% of all critical illness claims.2 For financial protection against these common illnesses3, choose our most affordable coverage.

Highlights

Lump-Sum Benefit: $25,000 to $2 million.

Comprehensive: Coverage for over 30 serious illnesses and conditions.4

Includes $10,000 accidental death benefit.

Convert term to permanent insurance without medical proof until age 71.

RBC Professional Series disability insurance

The Professional Series policy provides long-term disability coverage and return to work benefits that are designed around your unique needs.

Highlights

Total Disability Benefits: Receive a specified monthly benefit if illness or injury completely prevents you from working.4

Partial and Residual Disability Benefits: Makes your transition back to work easier if, as a result of injury or illness, you are only able to work part-time.

Choice of Benefit Periods: Receive benefits for two years, five years or until age 65.

Return to Work Assistance Benefits: Receive services that can help you get back to your job.

RBC payout annuities

RBC payout annuities can give you guaranteed income for life.

Highlights

Guarantee your retirement income.

Minimize your taxes.

Provide security to loved ones.

RBC segregated funds

Segregated funds give your money the chance to grow, while providing built-in guarantees to keep it safe.

Highlights

Guarantee your original investment.

Lock-in market gains.

Provide security to loved ones.

Protect your money from creditors.

Talk to an advisor if

-

You’re planning to combine multiple products.

-

You have unique health or family considerations.

-

You want a tailored financial plan.

Start online if

-

Your needs are straightforward.

-

You know the coverage type you want.

-

You want to get started now.

Helpful resources

How To Create the Right Retirement Plan For You

How much retirement income do you need? Planning for retirement requires careful consideration of your current and future financial needs. Here’s where to begin.

Worried you’ll outlive your retirement savings? Here are 3 reasons to consider payout annuities.

As some Canadians grow concerned if their savings will run out in retirement, payout annuities can help offer some financial stability.

Life insurance calculator

See how much coverage is right for you and your family.

Annuity calculator

Estimate your potential income from an annuity vs a RRIF.

Frequently asked questions for retirement planning

A comprehensive retirement plan will take into account your financial situation, your future needs and goals, and your tolerance and capacity for risk in your retirement years. A financial advisor should look at all of these factors when helping to guide you toward an income plan that’s right for you.

Some of the key factors you’ll want to discuss are:

- Your tolerance for risk in terms of market fluctuations

- Your investment goals when it comes to growth within your retirement fund

- Your desire for flexibility and liquidity versus your need for stability

- Your personal health and potential longevity; and

- Inflation and how it can affect your purchasing power during your retirement years

A financial advisor can support you in designing a plan that suits your needs and goals, whether it’s a straightforward strategy or a diversified approach to generating your retirement income.

One of the biggest retirement concerns is outliving your savings. Insurance products such as payout annuities can provide guaranteed income for life, which helps reduce this risk. They can be used alongside other sources of retirement income like pensions or registered savings plans to create more financial stability.

Yes. Segregated funds are actually ideal investment solutions for individuals who don’t qualify for life insurance. That’s because they offer death benefit guarantees that ensure your beneficiaries will receive a guaranteed percentage of your original investment (less any withdrawals and fees) upon your death. There is no medical checkup or underwriting required.

Portfolio solutions, such as RBC Select Guaranteed Investment Portfolios (GIPs) are designed to provide the right asset mix to meet your risk profile and investment objectives. Each RBC Select GIP is actively monitored and rebalanced by RBC Global Asset Management to ensure your investments remain on track. There are 4 RBC Select GIPs available, so whether you’re a conservative investor or more growth-oriented, you’re sure to find a portfolio that meets your needs.

As people get older, the likelihood of facing a serious health condition increases. Critical illness insurance can provide a lump-sum payment that helps cover expenses government or workplace benefits may not, such as medical costs or supplementing income if you need time to recover.

Critical illness insurance pays a one-time lump sum if you’re diagnosed with a covered condition, while disability insurance provides ongoing income replacement if you can’t work because of illness or injury.

Find insurance for all your needs

Building stability in retirement starts with planning today. The right coverage can help you enjoy peace of mind in the years ahead.

Canada.ca, Planning to save for retirement.

Munich Reinsurance Company, 2006 Critical Illness Survey.

Cancer is defined as a definite diagnosis of a tumour, which must be characterized by the uncontrolled growth and spread of malignant cells and the invasion of tissue. Types of Cancer include carcinoma, melanoma, leukemia, lymphoma, and sarcoma. The diagnosis of Cancer must be made by a specialist. The following forms of cancer are excluded: Lesions described as benign, pre-malignant, uncertain, borderline, non-invasive, carcinoma in-situ (Tis) or tumours classified as Ta; Malignant melanoma skin cancer that is less than or equal to 1.0 mm in thickness, unless it is ulcerated or is accompanied by lymph node or distant metastasis; Any non-melanoma skin cancer, without lymph node or distant metastasis; Prostate cancer classified as T1a or T1b, without lymph node or distant metastasis; Papillary thyroid cancer or follicular thyroid cancer, or both, that is less than or equal to 2.0 cm in greatest diameter and classified as T1, without lymph node or distant metastasis; Chronic lymphocytic leukemia classified less than Rai stage 1; or Malignant gastrointestinal stromal tumours (GIST) and malignant carcinoid tumours, classified less than AJCC Stage 2.

Certain conditions must be met for benefits to be payable. Your policy will provide complete details.