Important information:A potential Canada Post service disruption could take place within the coming weeks.

Important Information: A potential Canada Post service disruption could take place within the coming weeks.

In the event of a widespread postal disruption, you may not receive your insurance documents or be able to mail premium payments or documents to us. You are still responsible for making your insurance premium payments by your due date to maintain your insurance coverage.

While an accident can be overwhelming, it’s important to know how to protect yourself in the aftermath because post-accident scams are on the rise. Being aware of this type of fraud is the first step in protecting yourself against them.

But what does a post-accident scam look like?

It could mean getting towed to a repair shop that holds your car hostage until you pay an outrageous fee or even transfer ownership. In such an instance, fraudsters will intentionally cause an accident, and then demand that the vehicle be taken to a particular repair shop. They do so because it means the auto repair business is able to invoice all the repair work to a victim’s insurer. If you feel like this is about to occur, be sure to call your insurance provider to let them know what happened and how to proceed, including steps to arrange for tow truck service (if needed).

In some auto collision frauds, perpetrators may even claim for non-existent injuries after a collision. In short, if there is a way to get financial gain from a car accident where a fraudster looks like a victim, they will try to do so. That’s why it is so crucial to be vigilant to this type of crime and to know how to avoid insurance fraud. If at the scene of the accident, someone claims to be experiencing an injury be sure to call both the police and an ambulance right away for assistance. If the injury is real, then it’s best to have properly trained medical staff on hand, but if it’s part of an insurance scam, then having law enforcement at the scene of the accident can act as a deterrent to the fraudsters perpetuating their scam.

Insurers have seen customers fall victim to these fraudulent scams. Fortunately, these steps may help you avoid potential post-accident fraud:

Call your insurance provider right away once everyone’s safe. They’ll help you through the claims process smoothly.

Record details of the accident. Note the vehicles involved and the people or companies you interact with.

Don’t sign any blank forms or anything you don’t understand. Take time to read the fine print and ask questions.

Reach out to your insurer to discuss what options are available for repair shops and rental cars.

Finally, if you have suspicions of fraud, report it to your insurer.

By keeping to these steps, you may help keep yourself and your loved ones well-informed and protected against post-collision insurance scams.

Car accidents can be high-stress situations, but it’s still important to keep a level head during the post-collision process, so you can know when someone may be trying to pull a fast one on you. And remember, if you ever feel uncomfortable during your interactions with the other driver, you can always call the police to act as a neutral third party. Often, just their presence alone will be enough to deter any would be insurance scam artists.

Get Your Free Car Insurance Quote

Take a few minutes to get a competitive auto insurance quote online*

*Home and auto insurance products are distributed by RBC Insurance Agency Ltd. and underwritten by Aviva General Insurance Company. In Quebec, RBC Insurance Agency Ltd. Is registered as a damage insurance agency. As a result of government-run auto insurance plans, auto insurance is not available through RBC Insurance in Manitoba, Saskatchewan and British Columbia.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This is why it is important to always be prepared. Part of being prepared involves having an emergency kit.

Having an emergency kit in your car can be very helpful when you are in a bind. While some people overlook the importance of emergency kits because they rely on road side assistance, the reality is that you never know how long it will take for help to arrive.

What items should you include in your emergency kit?

While there is no limit to what items you can include in your emergency kit, there are a number of items that you may need to have. These items include:

A cell phone (if you don’t carry one with you)

First aid kit

Bottled water and snacks

A blanket, gloves, and additional warm clothing for the winter months

Flashlight and batteries

Tire gauge and Jumper cables

Small tool kit

Your emergency kit should have these items at a minimum, and depending on your specific situation, you may include other items. These additional items will be based on your driving frequency and the climate where you drive.

Regardless of how often and where you drive, having an emergency kit is common sense. If you don’t have one already, investing in one is not only important, it could be a lifesaver. This article is for general informational purposes only.

Get Your Free Car Insurance Quote

Take a few minutes to get a competitive auto insurance quote online*

*Home and auto insurance products are distributed by RBC Insurance Agency Ltd. and underwritten by Aviva General Insurance Company. In Quebec, RBC Insurance Agency Ltd. Is registered as a damage insurance agency. As a result of government-run auto insurance plans, auto insurance is not available through RBC Insurance in Manitoba, Saskatchewan and British Columbia.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

Remember to include the exterior of your home in that spring cleaning as well. Spring home cleaning is a tradition that serves a very useful purpose to tidy up your home and property of the build-up that has occurred during the cold weather.

The winter season brings a lot more headaches than cold weather and snow. Cold weather can damage the exterior of your house, cause water damage, and other home maintenance problems. Many of the effects of winter are noticed in the spring, and it’s important to take care of those home maintenance problems before they lead to serious exterior home and property damage.

Home maintenance checklist to prepare your house exterior for summer weather

When you start your spring cleaning, it is helpful to have a spring home maintenance checklist to help you know where to start and what home maintenance issues to look for.

Spring home maintenance tips

Here are four simple spring cleaning and home maintenance tips to help make exterior spring cleaning a breeze this year:

Inspect your house and property: Frozen ground can cause shifts in your landscaping and patios, which, if left unattended, can result in costly home repairs and injuries. Be sure to inspect your exterior walkways and driveways for cracks.

Remove debris from your gutters: Ensure that leaves and dirt are removed from your home gutters to prevent water blockage.

Repair damage to your roof: Replace missing or damaged shingles to prevent water from leaking through the roofs. Roof renovation may be necessary if there is extensive water damage.

Examine fences around your property: Ensure fences are still sturdy and lock properly to prevent injury and to help keep intruders from entering your yard, especially if you have a pool or water features.

Completing your spring home maintenance and exterior inspection

Make sure you follow proper safety standards and precautions in your community for any home maintenance work that is required. Where available and permitted, consider hiring an experienced local contractor to help with your spring home maintenance such as gutter cleaning and roof repairs.

By following these helpful tips and spring home maintenance checklist, you can identify potential risks to your home in advance and take action to help prevent more serious weather, water, and other damage to your home exterior.

Great Rates and Expert Advice on Home Insurance

Get a free online quote* for coverage to protect you, your property, and your belongings from the unexpected.

*Home and auto insurance products are distributed by RBC Insurance Agency Ltd. and underwritten by Aviva General Insurance Company. In Quebec, RBC Insurance Agency Ltd. Is registered as a damage insurance agency. As a result of government-run auto insurance plans, auto insurance is not available through RBC Insurance in Manitoba, Saskatchewan and British Columbia.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

A summer’s day can one minute be hot and sunny and with a blink of an eye, a storm can roll up with 45mph winds ripping through neighbourhoods or golf ball size hail, pounding down onto homes and vehicles causing physical damage to property.

Severe weather brings storm chasers and scammers who try to make an extra buck off your damaged property.

What are Property Damage Storm Chasers?

Storm chasers and scammers pose as legitimate property damage contractors, who often give false promises to repair property damage. Roof repair scams are an easy target when storms rip through neighbourhoods. It’s as easy as having a property contractor knock on your door, with a shingle in their hand, stating that they are doing work in the neighbourhood and noticed shingles missing off your roof.

Be aware and don’t be an easy target and fall for their claims!

How to Recognize Property Damage Storm Chasers

Here are some RED FLAGS to be aware of when identifying property repair scammers:

Exaggerating Damages – the dishonest property repair contractor will magnify the damages and lie to homeowners stating that the roof has an abundance of missing shingles. They will also often scare homeowners by stating that repairs need to be done ASAP or further damages, like water seeping into their homes, will occur on their property.

Contingent Agreements And Contracts – some cheating property repair contractors will promise the world to homeowners by advising they will be able to repair or replace full roofs. They will go as far as embellishing the truth to get homeowners to trust them into thinking they can help negotiate insurance claims. The contractor will provide a smooth-talking representative to persuade homeowners to sign documents and pressure them into using their business to repair the damage.

Upfront Payments – some corrupt property repair contractors will demand upfront cash payments and once the homeowner pays, the contractor disappears without finishing, or even starting the home repair.

Special Deals – some property repair scammers will offer deals or provide lower quotes. Cheaper doesn’t always mean better — remember the saying, “you get what you pay for.” Some contractors will low ball the property repair quote to get the job and once the work is done, homeowners are stuck with poor repairs and substandard materials.

Tips on how NOT to get scammed when having your property repaired:

Contact your insurance company. Your insurance company will be able to send a qualified contractor to assess damages and provide a reliable quote to have your property repaired.

Do your research — research the contractor and business online and ask for references.

Do not sign any documents until you have read the entire document thoroughly, including the fine print.

Check how long the contractor has been in business for and confirm their warranty.

Obtain more than one repair estimate.

Work with property repair contractors who are licensed and insured.

Great Rates and Expert Advice on Home Insurance

Get a free online quote* for coverage to protect you, your property, and your belongings from the unexpected.

*Home and auto insurance products are distributed by RBC Insurance Agency Ltd. and underwritten by Aviva General Insurance Company. In Quebec, RBC Insurance Agency Ltd. Is registered as a damage insurance agency. As a result of government-run auto insurance plans, auto insurance is not available through RBC Insurance in Manitoba, Saskatchewan and British Columbia.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

We hear all the time that life insurance is important and should be considered when planning our family’s financial future but, how do we know how much is enough? Understanding the different types of life insurance and itemizing what’s important to your family will help determine what coverage would be best for your needs. Here’s what you need to know.

You can arrange life insurance through an agent or broker, or in some cases through a group plan available through your employer or other organization.

Life insurance comes in several forms:

Term Life Insurance offers a simple insurance solution that protects your family for a set period of time. If you pass away during this time, your insurance policy pays your beneficiaries, tax-free.

Permanent Life Insurance gives you coverage for life and typically provides a death benefit with a savings/investment component. Two primary types of permanent life insurance are Universal Life Insurance and Whole Life Insurance.

Personal Accident Insurance is an affordable form of life insurance that protects your family if you pass away from an injury due to a sudden accident.

When you’re trying to figure out which type of life insurance you need, consider your current and future financial obligations. If you’re single with no children, your financial obligations might look quite different than a married couple with a mortgage, car payments and two small children.

How Much Life Insurance Do I Need?

There are many rules of thumb about how much life insurance is the right amount, but generally the amount depends on what you want it to cover. Putting pen to paper or using a handy tool can help you calculate how much life insurance you will need. Some helpful things to consider can include:

Providing for dependents until they’re finished post-secondary education.

Paying for a loved one’s nursing home expenses. These costs vary by province and can range anywhere from $1,475 to $6,000 per month.

Providing financial support for a spouse who is a home maker or stay at home parent.

Paying off your mortgage or other outstanding loans or debts.

Paying for funeral and burial costs which typically range from $7,000 – $15,000.

Once you’ve decided what items your life insurance policy should cover, think about your current annual income. If something were to happen to you, how many years of your current salary would your loved ones require to safely provide for their needs? That totaled amount should equal or be close to the amount you calculated that your life insurance policy should cover.

Do I Have Enough Life Insurance?

Once you’ve uncovered how much insurance your family will need, you’ll need to validate how much coverage you have already through work or a group plan to see if there are any gaps.

Make note of the type and amount of coverage you have through your employer provided group life insurance. A group life term insurance policy might cover just two or three times your annual salary. Depending on your goals, you might want to invest in additional life insurance of your own if the existing amount is not sufficient for your needs. Check the fine print in your employment benefits package, or contact your human resources department to help you find how much life insurance you have through work. If you switch jobs, your group policy will most likely end, so always stay up to date with your coverage. Consider taking out your own personal policy outside of your employer’s coverage to avoid ever being left without a policy.

Forecasting the future costs of providing for your family can be difficult on your own, but understanding these key points can help you feel more confident. If you need help estimating how much life insurance you might need, meet with an RBC Life Insurance Advisor or call us 1-866-223-71131-866-223-7113.

RBC Life Insurance

Protect Your Loved Ones With Dependable Life Insurance

*Home and auto insurance products are distributed by RBC Insurance Agency Ltd. and underwritten by Aviva General Insurance Company. In Quebec, RBC Insurance Agency Ltd. Is registered as a damage insurance agency. As a result of government-run auto insurance plans, auto insurance is not available through RBC Insurance in Manitoba, Saskatchewan and British Columbia.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

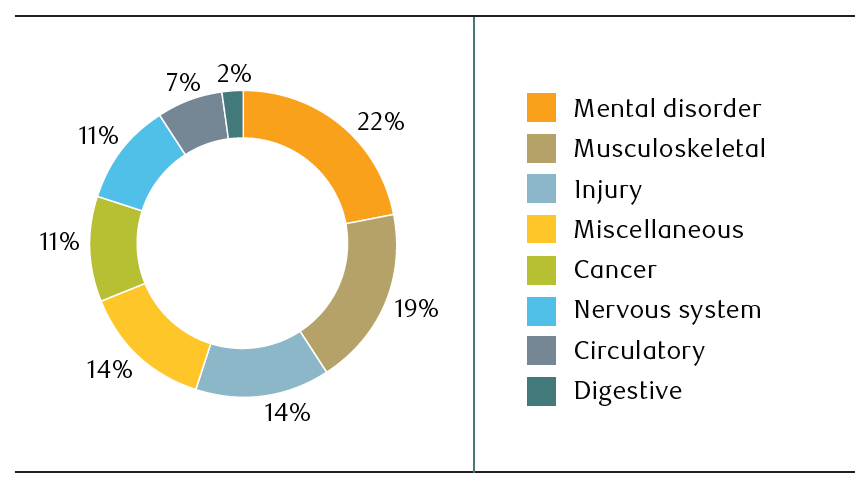

You need your pay cheque to pay your bills, do your extra-curricular activities, eat and so much more, so what happens if you suddenly become sick or injured and can’t work? If you’re a full-time employee, your benefits plan may provide some financial protection, in the form of disability insurance. You could even call disability insurance “Income replacement insurance” because it replaces some of your income if you get sick or injured and cannot work.

But is the coverage you have at work sufficient to meet your needs? We’ll break down disability insurance coverage that’s provided as part of employee benefits, and guide you through how to figure out whether your workplace plan fits your needs.

Disability insurance 101: Understanding the basics

Many people have short-term or long-term disability insurance coverage, or both, through group insurance provided by an employer.

*these numbers are based on disability insurance claims received by RBC Life Insurance Company® between 2014 and 2017.

Your benefit (or disability benefit), which is a term you’ll see used quite frequently below, is the payments you receive from your disability insurance policy. Short-term disability insurance policies usually provide benefits immediately and last between three and six months. Long-term policies, on the other hand, usually only provide benefits after a waiting period of one or more months, and then last for a specified period, like two years – or until you reach a specific age, such as 65. Short-term and long-term policies are designed to coordinate so you won’t be left with gaps in coverage.

Both forms of disability insurance provide some income replacement when you can’t work due to a disability, whether that’s from a physical injury, an illness, or a mental health condition. You can think of disability insurance as a form of insurance for your pay cheque, to keep income coming in even if you become disabled and can’t work.

1. How does my disability insurance policy protect my monthly income?

The details of how your insurance coverage protects your income will be set out directly in the policy. Reviewing the policy will tell you:

how much you will receive if you become disabled (usually between 60 to 85 percent of your monthly after-tax income)

the definition of “disability” used to qualify you for benefits

how long you will receive benefits for if you become disabled

what is the waiting period you need to complete (if any) to receive benefits

any limitations or exclusions preventing you from receiving benefits – like any pre-existing medical conditions, for example

A policy through work might offer an option to add extra coverage. This is considered a “top up” to your coverage. You might decide to add extra insurance if you find out that the standard monthly amount offered through your employee benefit plan is not enough to cover your monthly expenses.

Take some time to look through your budget so that you know what amount of income you need to have coming in every month to continue to cover your expenses.

2. How much monthly income could I receive from my disability insurance?

Your monthly income from a disability insurance policy will depend on your regular income amount, and how much of that income is replaced by your disability benefit.

Let’s say Sarah, age 34 and living in Ontario, earns $54,000 per year before tax – gross income. That’s $4,500 per month. The income protection policy offered by her employer replaces 60 percent of her salary, before tax, to a maximum of $5,000 per month if she becomes disabled.

If Sarah develops a disabling illness so that she can’t work and is eligible for a monthly disability benefit, she will receive 60 percent of $4,500 – or $2,700 – in monthly income. And because Sarah’s disability benefit of $2700 is less than the monthly maximum of $5,000, she will receive the full benefit for as long as she is eligible.

Sarah’s salary before taxes: $54,000

100% of pay cheque before need of disability benefit

60% of pay cheque with disability benefit

Monthly income before tax:

$4,500

$2,700*

*The $2700 benefit may or may not get taxed. That is dependent on whether Sarah pays the cost for her group disability coverage or if her employer pays. This will be discussed further below.

Do you know what percentage of your gross salary your employer disability insurance policy will cover? Do you know what the maximum per month benefit amount is? These are important questions to find out from your HR department or group plan administrator.

3. Who pays for my work disability insurance?

Often, employers will set up their employee benefits plan so the employee pays the full monthly cost for disability insurance. That’s usually because, if you pay, and not your employer, your disability benefits will be tax-free. This means your income while on disability would be closer to your take-home pay.

In contrast, if your employer pays for the cost of your disability insurance, you’d need to pay tax on your monthly disability benefit.

Do you pay for your disability insurance through work or does your employer? Will you be taxed on your employer disability benefit? This is an important question to ask your HR department or group plan administrator so you have the accurate monthly benefit amount for your budget calculations.

4. Will my disability insurance cheque be enough to meet my needs?

An important part of this puzzle to understand is how much of your after-tax income to you rely on to cover all your monthly expenses?

Note that if Sarah’s annual income was higher, her regular monthly income might already be above the maximum dollar amount her benefit will pay. This can put her at a disadvantage.

For example, if Sarah earned $120,000 gross per year, or around $10,000 per month before taxes, her disability coverage would only pay a maximum of $5,000 of monthly income – or 50 percent, not 60 percent, of her salary.

If this was Sarah’s situation, she might decide to purchase additional disability insurance, either through her employer or on her own.

5. Should I supplement the disability insurance policy I have through work?

Whether or not you have income protection as an employee benefit, you can also buy personal individual disability insurance from a broker or directly with an insurance company.

This way, you can get customized coverage for your needs, and you can choose the level and type of benefit you want. For example, after a specified period of receiving full benefits, most employer-provided disability insurance policies might may pay you only if you are unable to work in any capacity. In comparison, an individual policy might continue to pay for as long as you are unable to work at your own job.

Keep in mind, as well, that your employer-provided disability coverage is linked to your work, so if you stop working for that employer, your protection will end.

It’s important to take the time to ask your employer or HR department about the coverage you have. Once you have clarity about the kind of coverage you have in place, and you’ve calculated how much of your income you’ll need to have coming in to pay your monthly expenses, you’ll be in a position to make an informed choice about whether your existing coverage is enough.

*Home and auto insurance products are distributed by RBC Insurance Agency Ltd. and underwritten by Aviva General Insurance Company. In Quebec, RBC Insurance Agency Ltd. Is registered as a damage insurance agency. As a result of government-run auto insurance plans, auto insurance is not available through RBC Insurance in Manitoba, Saskatchewan and British Columbia.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

Most Canadians are fortunate to have provincial medical coverage for hospital visits, outpatient services and prescription drug costs incurred in-province or in-country. All provinces and territories except Quebec have a billing agreement that provides coverage for insured hospital and physician services, but some plans have exceptions.

Want to know how much out-of-province medical coverage your province or territory provides?

For more in-depth and up to date information regarding out of province coverage visit your province’s approved health insurance website. Understanding the coverage you have before you travel is an important part of planning a trip.

Alberta

Plan: Alberta Health Care Insurance Plan (AHCIP)

Details: AHCIP provides coverage for insured physicians and hospital costs in other provinces across Canada. This means that in most cases when you present your AHCIP card to a medical or hospital service provider in another province, there is no cost to you. If you visit a physician in Quebec, you may have to pay up front, but can submit a receipt to AHCIP to be reimbursed. If you use a private facility you will have to pay facility fees including laboratory services, MRIs and accommodation.

There is limited coverage for physician and hospital costs outside of Canada. For expenses incurred out-of-country, AHCIP will cover a maximum of $100/day for hospital services, and a maximum of $50/day for outpatient services. Travelers are responsible for paying the health service provider first and then can submit a claim to the AHCIP office to request reimbursement for eligible out-of-country health expenses. The traveler is responsible for paying the difference between the amount charged and the amount AHCIP reimburses.

British Columbia

Plan:Medical Service Plan (MSP)

Details: British Columbia’s MSP will help pay for unexpected medical services outside of the province if they are normally insured by MSP. Reimbursement for physician services will be made in Canadian funds and any excess cost is the responsibility of the beneficiary. When travelling to Quebec or outside of Canada, you will probably be required to pay out of pocket for medical services and then get reimbursement after.

MSP does not provide any coverage for treatment provided by a non-physician health care practitioner (e.g., physician assistant, nurse practitioner, chiropractor or physical therapist), prescription drugs, medical supplies or ambulance services outside the province. The province will pay up to $75/day for emergency hospital services outside of Canada.

Manitoba

Plan: Manitoba Health, Seniors and Active Living (MHSAL)

Details:Manitobans who travel to another province are still covered by MHSAL if they present their Manitoba Health card to a hospital or other medical care centre.

Travellers admitted on an emergency basis to a hospital outside of Canada are covered by MHSAL for services, based on established daily rates but are responsible for some of the costs. Care received as a hospital outpatient or from an emergency room outside of Canada is covered up to $100/visit. Physician services are covered at the same rates paid to Manitoba doctors.

New Brunswick

Plan: Medicare

Details: New Brunswick Medicare will cover insured physician or hospital services in all provinces and territories, except for Quebec, upon presentation of a Medicare card.

The plan will cover only emergency out-of-country physician and hospital services with prior approval, at a maximum of $100/day for in-patient services and $50/day for outpatient services.

Newfoundland & Labrador

Plan: Medical Care Plan (MCP)

Details: Provides limited coverage for travellers under the Medical Care Plan (MCP) and the Hospital Insurance Plan. MCP covers only insured services and does not cover all charges related to hospitals and clinics or ambulance/air ambulance services inside or outside of Canada. Individuals who leave the province for more than 30 days will need an out-of-province coverage certificate.

Nova Scotia

Plan: Medical Services Insurance (MSI)

Details: MSI will provide coverage to Nova Scotia residents for medical expenses incurred anywhere in the country, upon presentation of a valid health card, except Quebec for physician services.

For out-of-country medical care, MSI will cover emergency medical services only, at Nova Scotia rates. The current rate for emergency in-patient services in-province is $525 a day, plus 50 percent of ancillary fees incurred during an in-patient stay. The program will not cover ambulance services, Pharmacare, children’s dental programs, routine vision analysis, or any out-patient charges, including X-ray, diagnostic tests and laboratory charges.

Ontario

Plan: Ontario Health Insurance Plan (OHIP)

Details: OHIP will cover physician and hospital services outside of the province upon presentation of a valid health card. Physicians outside of Ontario can choose to bill the province directly, in which case the patient doesn’t pay anything, or to bill the patient, who will be reimbursed upon submitting appropriate documents and invoices to OHIP.

Details: Island residents are covered for medical emergencies or sudden illness anywhere in Canada, at PEI rates. Costs incurred for non-emergency care received outside of the province are not covered without prior approval from Health PEI.

When travelling outside of Canada, coverage is available for emergency or sudden illness up to a set amount. The difference between the medical fees charged and the amount that Health PEI will pay is the responsibility of the traveler.

Québec

Plan: Régie de l’assurance maladie Québec (RAMQ)

Details: Québec residents who hold a valid health insurance card can receive out-of-province health care services under the Québec Health Insurance Plan (RAMQ), but in most cases, RAMQ reimburses only part of the cost. For example, a patient seeking hospital services in Ontario totaling $928 will be reimbursed only $422. The patient is responsible for paying the difference.

For out-of-country expenses, RAMQ will cover a maximum of $100/day for hospital services and a maximum of $50/day for outpatient services. For hemodialysis and the required medication, RAMQ will cover up to $220/treatment, regardless of whether the cardholder is hospitalized.

Saskatchewan

Plan: Saskatchewan Health

Details: The province provides coverage for physician and hospital care across Canada upon presentation of a valid health card. Travelers to Quebec may have to pay for physician services then submit a bill to the Ministry of Health for reimbursement at Saskatchewan rates.

For out-of-country care, Saskatchewan Health will provide limited coverage from approved hospitals at Saskatchewan rates, and only if the same services would be covered in-province. Saskatchewan Health will cover a maximum of $100/day for hospital services and a maximum of $50/day for outpatient services.

Yukon

Plan: Yukon Health Care Insurance Plan (YHCIP)

Details: YHCIP provides basic coverage for hospital and physician services from publicly funded hospitals inside or outside of Canada, at Yukon rates. There are limitations within this coverage.

YHCIP does not provide coverage for air or ground ambulance services or any related services, such as hospital transfer, escorts or return transportation charges, regardless of where the expenses are incurred.

It’s important to note that non-physician (e.g., physician assistant, nurse practitioner) and non-hospital (e.g., chiropractic, dental care) services are not covered under most provincial plans.

For more in-depth and up to date information regarding out of province coverage visit your province’s approved health insurance website. Understanding the coverage you have before you travel is an important part of planning a trip.

When you are ready to get away, RBC Insurance will be there to help you with your travel insurance needs. Click to get a travel insurance quote.

RBC Travel Insurance

If you need help during your trip for a medical or other travel emergency, help is available 24/7.

*Home and auto insurance products are distributed by RBC Insurance Agency Ltd. and underwritten by Aviva General Insurance Company. In Quebec, RBC Insurance Agency Ltd. Is registered as a damage insurance agency. As a result of government-run auto insurance plans, auto insurance is not available through RBC Insurance in Manitoba, Saskatchewan and British Columbia.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.