Home > Health Insurance > Affordable Disability Insurance for Canadians

Disability insurance for Canadians

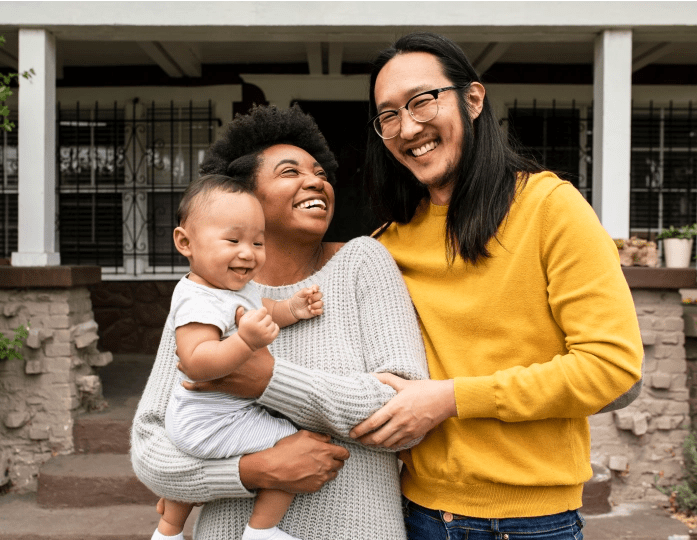

Your provincial health plan can help with the medical bills. But to replace lost income, you need disability insurance.

Note: Online quote is for RBC Simplified Disability Insurance only.

Protect your income and your lifestyle with affordable disability insurance

Protect your income if an injury, illness or mental health event stops you from working. Explore our straightforward, affordable options that can fill the coverage gaps with other disability benefits so that you can get back to work faster.

Benefits of disability illness insurance

Flexible options

Our disability insurance plans offer a range of options to choose from, including the

Family compassionate care rider

An option to help you care for a loved one with a terminal diagnosis15

The Family Compassionate Care Rider is a first-of-its-kind option that gives you financial support as you navigate a spouse or child’s (Spouse or child of any age)16 terminal illness or injury.

Ideal if You

- Want the flexibility to take time off, work reduced hours or continue working in the event of your spouse or child’s terminal diagnosis

Highlights

- No Waiting Period17: Your benefits start the day of your loved one’s diagnosis, so you can focus on spending time with them.

- Flexibility and Choice: You can choose how to use your payments—cover medical bills and travel expenses, pay for child care, and/or supplement income.

What’s covered?

- Up to 12 months of benefit payments: Amount is equal to your policy’s maximum monthly disability benefit

Who can apply?

The Family Compassionate Care Rider is available as an option on the following RBC Disability Insurance products:

- The Professional Series

- The Foundation Series

- The Bridge Series

- Quantum

Additional information

- May only be added to new disability insurance policies

- Cannot be purchased as a standalone product

- Not available with Wage Loss Replacement Plans

, a first-of-its-kind.

Fills coverage gap

Canada Pension Plan (CPP) and Quebec Pension Plan (QPP) disability benefits are limited and may be more restrictive.

Helps you return to work1

Many of our plans provide return to work benefits such as rehabilitation, job retraining and other services to help you get back to work.

Portable

Most employer-sponsored plans end if you leave your job. A disability insurance plan from RBC Insurance can go with you.

Types of disability insurance

-

For tradespeople and part-time workers

-

For high-income earners & executives

-

For small business owners & skilled workers

-

For retirement planning

Need help choosing? Compare your options here.

For tradespeople & part-time workers

Disability insurance

The Fundamental Series™

The Fundamental Series™ policy offers injury-only coverage that is easy to qualify for and a simple application for illness coverage.1

Ideal if you

Are self-employed

Are a contract or seasonal worker

Are a tradesperson or construction worker

Are a self-employed farmer

Work in retail

Highlights

Easy to Qualify: Answer 3 pre-qualifying questions to apply for injury-only coverage.

Optional Illness Coverage: Complete a short application to apply for illness coverage.

Total Disability Benefit: Receive a monthly benefit if illness or injury11 completely prevents you from working12.

Partial Disability Benefit: Receive a specified monthly benefit if illness or injury11 prevents you from working full-time12.

Return to Work Assistance Benefits: Receive services that can help you get back to your job.

- Choice of Benefit Periods: Choose two years (illness coverage), five years or to age 70.

- Guaranteed Renewable: We cannot cancel the policy without your consent, up until you turn age 75 (injury coverage) or age 70 (illness coverage). Premiums may be subject to change; however, we cannot change your premiums unless we do so for an entire group of policyholders sharing similar characteristics.

- Accidental Medical Emergency Reimbursement Benefit: Helps cover certain medical expenses not covered by government health insurance plans.

- Waiver of Premium During Disability: Your premiums will be waived if you are disabled and being paid monthly benefits.

- Medical Confidence™ Service7: Receive faster access to care and treatment by appropriate physician specialists, a more accurate diagnosis, one-on-one support from a Registered Nurse and more.

- Portable: You can keep your policy if you change jobs.

Who can apply?

Ages 18-64 (for illness coverage)

Ages 18-69 (for injury coverage)

Canadian citizens

Permanent residents/landed immigrants who are not planning to relocate out of Canada in the next 24 months

What’s covered?5

First 36 months of disability: You are considered totally disabled if, due to injury or illness (if illness coverage was purchased), you are:

- Unable to perform the important duties of your regular occupation, and

- Not engaged in any other gainful occupation, and

- Receiving appropriate physician’s care

After 36 months of disability: You continue to be considered totally disabled if, due to injury or illness, you are:

- Unable to engage in any reasonable occupation for which you are, or may reasonably become, fitted by education, training or experience, and

- Receiving appropriate physician’s care

Partial disability is described as follows:

- You are not totally disabled, and

- You are engaged in your regular occupation or any gainful occupation, and

- Due directly to continuing injury or illness (if illness coverage was purchased), you are unable to perform either:

- One or more important duties of your regular occupation, or

- The important duties of your regular occupation at least one-half of the time normally required; and

- You are receiving a physician’s care

Partial benefits are 50% of your total disability benefit and are payable for up to six months.

If you have emergency medical expenses because of an accidental injury and you provide us with proof of payment for the expenses, we will reimburse you up to $10,000 for the reasonable and customary amounts of those expenses.

Customized return to work benefits provide financial benefits, as well as rehabilitation, retraining, work-site modifications and other services to assist you in returning to full-time work.

This is the number of days between the onset of a disability and the day you begin receiving benefits. You can choose from: 0, 30, 90 or 120 days for injury coverage and 30, 90 or 120 days for illness coverage.

Choose from the following optional coverage (subject to eligibility):

- 24-Hour Coverage Benefit: This policy is non-occupational, which means it covers you when you are not working. If you choose this benefit, you will be covered 24 hours a day, at work, as well as outside of work. You may wish to purchase this optional benefit if you do not have workers’ compensation or similar coverage.

- Illness Coverage: Apply for an amount up to your equivalent monthly injury benefit.

- Accidental Death and Dismemberment Benefit: If you sustain an accidental injury as outlined in your policy, or if you die as a result of an accident, you or your beneficiaries receive a specified benefit based on the type of injury.

- Business Overhead Expense Benefit: Reimburses you for certain business overhead expenses (rent, utilities, salaries, etc.) if you become totally disabled and meet the conditions outlined in your policy.

We will not pay monthly benefits nor waive premiums for any period of disability that results, directly or indirectly, from:

- Flying in an aircraft that is not a certified passenger aircraft operated by a properly certified pilot

- Participating in professional athletics or underwater activities, including scuba diving

- Engaging in certain dangerous activities such as mountaineering, indoor or outdoor rock climbing, caving, parachuting, sky diving, hang gliding, bungee jumping and racing

- Operating a motor vehicle while under the influence of any intoxicant or while you have a blood alcohol concentration in excess of 80 mg of alcohol per 100 ml of blood

- Self-inflicted harm or attempted suicide

- Committing a criminal offence

- Drugs and narcotics

- Riots or acts of war

- Pregnancy and childbirth

- Infections related to AIDS and HIV

- Subjective conditions (e.g. fibromyalgia, chronic fatigue syndrome)

- Mental and nervous disorders

- Participation in the armed forces

This policy also contains limitations related to:

- Back and neck injuries

- Degenerative disc disease

- Soft tissue injuries

We also will not pay monthly benefits nor waive premiums for any:

- Period of time you are in a jail, under house arrest, or otherwise incarcerated

- Injury sustained or illness which first manifests itself before your policy becomes effective or while your policy is not in force

About your premiums

Premiums are subject to change (can only be changed if we do so for an entire group of policyholders sharing similar characteristics)

Pay no premiums while you’re collecting benefits

As long as you pay your premiums as required, we cannot cancel the policy without your consent, up until you turn age 75 (injury coverage) or age 70 (illness coverage)

- Policy is non-cancellable to age 65

- After age 65, it is renewable for life if your premiums are paid as required

- Rates and benefit periods are subject to change after age 65

Your renewal options after age 65 are:

- Up to age 75 and while employed full-time in a gainful occupation, you may continue the policy with a total disability benefit only with a maximum benefit period of 24 months. After age 75, the maximum benefit period is 12 months.

- If not employed full-time, you may elect a $100 per day benefit payable while confined to a hospital. The maximum benefit period for hospitalization is six months.

Policy documents:

The information above is intended as a summary only.

Disability insurance

The Bridge Series®

An affordable plan with numerous options to give you the right coverage. The Bridge Series® policy offers disability benefits, return to work assistance and options similar to The Foundation Series™ policy, but at a lower cost.

Ideal if you

Are a small business owner or manager

A tradesperson

A farmer

A middle-income earner

Highlights

Total disability benefits: Receive a specified monthly benefit if illness or injury completely prevents you from working.5

Choice of benefit periods: Receive benefits for two years, five years, or until age 65.

Return to work assistance benefits: Receive services that can help you get back to your job.

- Guaranteed Renewable: We cannot change or cancel the policy without your consent, up until you turn 65. Premiums are level, but may be subject to change. However, we cannot change your premiums unless we do so for an entire group of policyholders sharing similar characteristics.

- Medical Confidence™ Service7: Receive faster access to care and treatment by appropriate physician specialists, a more accurate diagnosis, one-on-one support from a Registered Nurse and more.

- Long-term Care Conversion Option: From age 55 to 65, you can convert all or some of your coverage to long-term care insurance, without providing evidence of good health.8

- Waiver of Premium During Disability: Your premiums will be waived if you are disabled and being paid monthly benefits.

- Portable: You can keep your policy if you change jobs.

Who can apply?

Ages 18-60

Canadian citizens

Permanent residents/landed immigrants

In some cases, individuals working part-time or new business owners may be eligible

Are you a farmer? Ask about enhanced guidelines for proprietors of farms.

What’s covered?5

The policy pays a total disability benefit as follows:

- First 24 months of disability: Subject to some limitations, you are considered totally disabled if, due to injury or illness, you are:

- Unable to perform the essential duties of your regular occupation, and

- Not engaged in any other gainful occupation, and

- Receiving appropriate physician’s care

(This is the “regular occupation” definition of disability.)

- After 24 months of disability: You continue to be considered totally disabled if, due to injury or illness:

- With any reasonable assistance or modification of job duties and subject to some limitations, you are unable to perform the essential duties of any occupation for which you are reasonably fitted by education, training or experience, considering your prior economic status, and

- You are not working in a gainful occupation, and

- You are receiving appropriate physician’s care

Note: You can purchase the optional Regular Occupation Extension Benefit rider to extend the “regular occupation” definition of disability above from 24 months to the end of your benefit period.

Customized return to work benefits provide financial benefits, as well as rehabilitation, retraining, work-site modifications and other services to assist you in returning to full-time work.

If you die prior to age 65 while receiving total disability benefits, your beneficiary will receive a payment for three times the maximum monthly benefit payable at the time of death.

To ensure your benefits are coordinated with other sources of income received during disability, the policy includes an integration of benefits provision. If the sum of current earnings and other income or disability benefits exceeds 85% of your pre-disability income, then your payable benefits for disability will be reduced by that amount.

This is the number of days between the onset of a disability and the day you begin receiving benefits. You can choose from: 30, 60, 90, 120 and 180 days. (360 and 720 days are also available to some occupational classes. The two-year benefit period is not available with a 720-day elimination period.)

Choose from the following optional coverage (subject to eligibility):

- Family Compassionate Care Rider: The Family Compassionate Leave rider provides a monthly benefit to insureds whose spouses or children are diagnosed with a terminal illness. The benefit matches the basic indemnity on the disability policy of the insured, and can continue to the earlier of 12 months of the death of the insured’s family member. Premiums on the disability policy are waived while the benefit is being paid. *Not available with Wage Loss Replacement Plans

- Regular Occupation Extension Benefit: Extend the regular occupation definition of disability from 24 months to the end of the benefit period. This ensures that you receive full benefits if you can’t work in your regular occupation, provided you are not engaged in any gainful occupation and are receiving a physician’s care.

- Short-Term Partial Disability Benefit: Receive 50% of the total disability benefit for up to 12 months if you are partially disabled.

- Long-Term Partial Disability Benefit: If you are partially disabled, receive 50% of the total disability benefit for the first 24 months and 25% of the total disability benefit for the duration of the benefit period.

- Future Income Option: To keep pace with your rising income, this allows you to purchase additional coverage on each policy anniversary date, up to age 55, without having to prove your health status.

- Cost of Living Benefit: While you are disabled, this benefit protects you against inflation, subject to limits.

- Retirement Protector Rider: Helps you maintain deposits to a retirement savings plan (RSP) while you are totally disabled.

- Hospitalization Benefit: Subject to certain limitations, after you have been hospitalized for 24 consecutive hours, you will receive a benefit for every day you are hospitalized. You will also receive an additional benefit four times the daily hospital benefit while you are in an intensive care unit.

Benefits are not paid for disabilities due to:

- An act or accident of war

- Normal pregnancy or childbirth (complications of pregnancy or childbirth are covered)

- Any injury sustained or illness which first manifests itself before your policy becomes effective or while your policy is not in force

- Opportunistic infections or other illnesses that physicians commonly associate with Acquired Immune Deficiency Syndrome (AIDS) or the Human Immunodeficiency Virus if you had either AIDS or HIV prior to the issue date of your policy

- 24 month limitation for mental, psychiatric or emotional disorders

- 24 month limitation for soft tissue injuries, degenerative disc disease and specified chronic diseases.

In addition, the policy won’t pay a benefit for any period during which you are incarcerated.

About your premiums

Pay level premiums, which are subject to change (can only be changed if we do so for an entire group of policyholders sharing similar characteristics)

Pay no premiums while you’re collecting benefits

- Guaranteed renewable to age 65 (policy can’t be changed or canceled without your consent)

- After age 65, while you are employed full-time in a gainful occupation, you may continue the policy for total disability only

- The maximum benefit period after age 65 in 24 months

Policy documents:

The information above is intended as a summary only.

For high-income earners & executives

Disability insurance

The Professional Series®

The Professional Series® policy provides long-term disability coverage and return to work benefits that are designed around your unique needs.

Ideal if you

Need a higher level of income protection

Are a business owner, executive, doctor, lawyer, accountant, etc.

Highlights

Total Disability Benefits: Receive a specified monthly benefit if illness or injury completely prevents you from working6.

Partial and Residual Disability Benefits: Makes your transition back to work easier if, as a result of injury or illness, you are only able to work part-time.

Choice of Benefit Periods: Receive benefits for two years, five years or until age 65.

Return to Work Assistance Benefits: Receive services that can help you get back to your job.

- Non-Cancellable: We cannot change the policy or premiums, or cancel the policy without your consent, up until you turn age 65. (Rates and benefit periods are subject to change after age 65.)

- Recovery Benefit: Pays a portion of your monthly benefit for up to four months during your initial return to full-time work after a total or residual disability (two months for a partial disability), if you have a 20% or more decrease in earnings.

- Medical Confidence™ Service7: Receive faster access to care and treatment by appropriate physician specialists, a more accurate diagnosis, one-on-one support from a Registered Nurse and more.

- Long-Term Care Conversion Option: From age 55 to 65, you can convert all or some of your coverage to long-term care insurance, without providing evidence of good health.

- Waiver of Premium During Disability: Your premiums will be waived if you are disabled and being paid monthly benefits.

- Health Care Profession Rider: If you are a qualified health care professional, you will receive this rider at no additional cost. If you become HIV-impaired or hepatitis-impaired and, due to your impairment, you meet one of the conditions of the rider, you will be considered disabled.

- Portable: You can keep your policy if you change jobs.

Who can apply?

Ages 18-60

Canadian citizens

Permanent residents/landed immigrants

What’s covered?5

Choose to receive benefits for two years, five years or until age 65.

- The plan provides benefits for three definitions of disability: total disability, partial disability and residual disability.

- Total disability benefits: Payable if, as a result of injury or illness, you are:

- Unable to perform the important duties of your regular occupation, and

- Not engaged in any gainful occupation, and

- Receiving appropriate physician’s care

- Partial disability benefits: To meet the definition of partial disability, you must not be totally disabled and must be engaged in your regular occupation or another job at the time of partial disability. You are considered partially disabled if, due directly to injury or illness, you are:

- Unable to perform one or more of the important duties of your regular occupation or the important duties of your occupation at least one-half of the time normally required, and

- Receiving appropriate physician’s care

Eligibility for partial disability benefits is based on the loss of time or your inability to perform your duties as a result of injury or illness. The benefit is payable up to the end of your benefit period with 50% of the maximum monthly benefit payable for the first 24 months and 25% payable for the remainder of the benefit period.

- Residual disability benefits: To meet the definition of residual disability, you must not be totally disabled and must be engaged in your occupation or other job at the time of residual disability. You are considered residually disabled if you have a loss of earnings of at least 20% and are receiving appropriate physician’s care.

Eligibility for residual disability benefits is based on a loss of earnings as a result of injury or illness. A proportionate benefit is payable based on your percentage of lost earnings.

Note: At any one time during a partial disability, you may switch to residual disability benefits. In addition, you will be reimbursed for any additional residual disability benefit you would have received during the 12 months prior to switching.

Customized return to work benefits provide financial benefits, as well as rehabilitation, retraining, work-site modifications and other services to assist you in returning to full-time work.

If you die prior to age 65 while receiving total disability benefits, your beneficiary will receive a payment for three times the maximum monthly benefit payable at the time of death.

This is the number of days between the onset of a disability and the day you begin receiving benefits. You can choose from the following: 30, 60, 90, 120, 180, 365 or 730 days. (The two-year benefit period is not available with a 730-day elimination period.)

Choose from the following optional coverage (subject to eligibility)5:

- Family Compassionate Care Rider: The Family Compassionate Leave rider provides a monthly benefit to insureds whose spouses or children are diagnosed with a terminal illness. The benefit matches the basic indemnity on the disability policy of the insured, and can continue to the earlier of 12 months of the death of the insured’s family member. Premiums on the disability policy are waived while the benefit is being paid. *Not available with Wage Loss Replacement Plans

- Additional Monthly Benefits: Adds more coverage to your base coverage.

- Future Income Option: To keep pace with your rising income, this allows you to purchase additional coverage on each policy anniversary date, up to age 55, without having to prove your health status.

- Cost of Living Benefit: While you are disabled, this benefit protects you against inflation, subject to limits.

- Disability in Your Occupation Benefit: Enhances your policy’s definition of total disability to disregard participation in other occupations while you are totally disabled in your primary occupation.

- Retirement Protector Rider: Helps you maintain deposits to a retirement savings plan (RSP) while you are totally disabled.

- First Day of Hospitalization Benefit: Waives the waiting period for total disability as long as you satisfy the policy’s definition of total disability and have been hospitalized for 72 consecutive hours. This ensures payment of the total disability benefit from the first day of hospitalization.

- Accidental Death and Dismemberment Benefit: If you sustain an accidental injury as outlined in your policy, or if you die as a result of an accident, you or your beneficiaries receive a specified benefit based on the type of injury.

Benefits are not paid for disabilities due to:

- An act or accident of war

- Normal pregnancy or childbirth (complications of pregnancy or childbirth are covered)

- Any injury sustained or illness which first manifests itself before your policy becomes effective or while your policy is not in force

In addition, the policy won’t pay a benefit for any period during which you are incarcerated.

About your premiums

Choose from two premium options:

Level premiums guaranteed to age 65 (we cannot change your premiums)

Step rate premiums (ages 18-35 only), which let you pay less while you’re getting your career off the ground (guaranteed to age 65)

Pay no premiums while you’re collecting benefits

- Policy is non-cancellable to age 65

- After age 65, it is renewable for life if your premiums are paid as required

- Rates and benefit periods are subject to change after age 65

Your renewal options after age 65 are:

- Up to age 75 and while employed full-time in a gainful occupation, you may continue the policy with a total disability benefit only with a maximum benefit period of 24 months. After age 75, the maximum benefit period is 12 months.

- If not employed full-time, you may elect a $100 per day benefit payable while confined to a hospital. The maximum benefit period for hospitalization is six months.

Policy documents:

The information above is intended as a summary only.

For small business owners & skilled workers

Disability insurance

The Foundation Series™

The Foundation Series™ policy provides total disability benefits and broad return to work assistance. Offering flexible options, we can design a policy to fit your needs and budget.

Ideal if you

Are a small business owner or manager

A tradesperson

A farmer

A middle-income earner

Highlights

Total disability benefits: Receive a specified monthly benefit if illness or injury completely prevents you from working.5

Choice of benefit periods: Receive benefits for two years, five years, or until age 65.

Return to work assistance benefits: Receive services that can help you get back to your job.

- Non-Cancellable: We cannot change the policy or premiums, or cancel the policy without your consent, up until you turn age 65. (Rates and benefit periods are subject to change after age 65.)

- Medical Confidence™7: Receive faster access to care and treatment by

appropriate physician specialists, a more accurate diagnosis, one-on-one support from a Registered Nurse and more. - Long-Term Care Conversion Option: From age 55 to 65, you can convert all or some of your coverage to long-term care insurance, without providing evidence of good health.

- Waiver of Premium During Disability: Your premiums will be waived if you are disabled and being paid monthly benefits.

- Health Care Profession Rider: If you are a qualified health care professional, you will receive this rider at no additional cost. If you become HIV-impaired or hepatitis-impaired and, due to your impairment, you meet one of the conditions of the rider, you will be considered disabled.

- Portable: You can keep your policy if you change jobs.

Who can apply?

Ages 18-60

Canadian citizens

Permanent residents/landed immigrants

Are you a farmer? Ask about enhanced guidelines for proprietors of farms.

What’s covered?5

The policy pays a total disability benefit as follows:

- First 24 months of disability: Subject to some limitations, you are considered totally disabled if, due to injury or illness, you are:

- Unable to perform the essential duties of your regular occupation, and

- Not engaged in any other gainful occupation, and

- Receiving appropriate physician’s care

(This is the “regular occupation” definition of disability.)

- After 24 months of disability: You continue to be considered totally disabled if, due to injury or illness:

- With any reasonable assistance or modification of job duties and subject to some limitations, you are unable to perform the essential duties of any occupation for which you are reasonably fitted by education, training or experience, considering your prior economic status, and

- You are not working in a gainful occupation, and

- You are receiving appropriate physician’s care

Note: You can purchase the optional Enhanced Definition of Disability Benefit rider to extend the “regular occupation” definition of disability above from 24 months to the end of your benefit period.

Customized return to work benefits provide financial benefits, as well as rehabilitation, retraining, work-site modifications and other services to assist you in returning to full-time work.

If you die prior to age 65 while receiving total disability benefits, your beneficiary will receive a payment for three times the maximum monthly payable at the time of death.

If you receive any benefits related to your disability under your auto insurance coverage, your disability benefits will be reduced by that amount.

This is the number of days between the onset of a disability and the day you begin receiving benefits. You can choose from: 30, 60, 90, 120 and 180 days. (360 and 720 days are also available to some occupational classes. The two-year benefit period is not available with a 720-day elimination period.)

Choose from the following optional coverage (subject to eligibility):

- Family Compassionate Care Rider: The Family Compassionate Leave rider provides a monthly benefit to insureds whose spouses or children are diagnosed with a terminal illness. The benefit matches the basic indemnity on the disability policy of the insured, and can continue to the earlier of 12 months of the death of the insured’s family member. Premiums on the disability policy are waived while the benefit is being paid. *Not available with Wage Loss Replacement Plans

- Additional Monthly Benefits: Adds more coverage to your base coverage.

- Enhanced Definition of Disability Benefit: Extend the regular occupation definition of disability from 24 months to the end of the benefit period. This ensures that you receive full benefits if you can’t work in your regular occupation, provided you are not engaged in any gainful occupation and are receiving a physician’s care.

- Partial Disability Benefit: Receive a portion of your total disability benefit if you are partially disabled, as defined by the policy.

- Future Income Option: To keep pace with your rising income, this allows you to purchase additional coverage on each policy anniversary date, up to age 55, without having to prove your health status.

- Cost of Living Benefit: While you are disabled, this benefit protects you against inflation, subject to limits.

- Retirement Protector Rider: Helps you maintain deposits to a retirement savings plan (RSP) while you are totally disabled.

- First Day of Hospitalization Benefit: Waives the waiting period for total disability as long as you satisfy the policy’s definition of total disability and have been hospitalized for 72 consecutive hours. This ensures payment of the total disability benefit from the first day of hospitalization.

- Accidental Death and Dismemberment Benefit: If you sustain an accidental injury as outlined in your policy, or if you die as a result of an accident, you or your beneficiaries receive a specified benefit based on the type of injury.

Benefits are not paid for disabilities due to:

- An act or accident of war

- Normal pregnancy or childbirth (complications of pregnancy or childbirth are covered)

- Any injury sustained or illness which first manifests itself before your policy becomes effective or while your policy is not in force

In addition, the policy won’t pay a benefit for any period during which you are incarcerated.

About your premiums

Level premiums guaranteed to age 65 (we cannot change your premiums)

Step rate premiums (ages 18-35 only), which let you pay less while you’re getting your career off the ground (guaranteed to age 65)

Pay no premiums while you’re collecting benefits

Your renewal options after age 65 are:

- Policy is non-cancellable to age 65

- After age 65, it is renewable for life if your premiums are paid as required

- Rates and benefit periods are subject to change after age 65

Policy documents:

The information above is intended as a summary only.

Disability insurance

Quantum®

The Quantum® policy offers quality disability coverage and return to work benefits in case an injury or illness causes you to lose 20% or more of your earnings.

Ideal if you

Need a higher level of income protection

Are a business owner, executive, doctor, lawyer, accountant, etc or a fee-for-service professional.

Want quality disability coverage similar to the Professional Series, but that takes a different approach to providing long-term individual disability income protection

Highlights

Disability Benefits: Receive a specified monthly benefit if illness or injury reduces your ability to work and causes at least a 20% loss of earnings.

Choice of Benefit Periods: Receive benefits for two years, five years, or until age 65.

Return to Work Assistance Benefits: Receive services that can help you get back to your job.

- Guaranteed Renewable: We cannot change or cancel the policy without your consent, up until you turn 65. Premiums are level, but may be subject to change. However, we cannot change your premiums unless we do so for an entire group of policyholders sharing similar characteristics.

- Recovery Benefit: Pays a portion of your monthly benefit for up to 12 months if you are no longer disabled, are able to work in a reasonable occupation, have a 20% or more decrease in prior earnings and meet the other conditions of the policy.

- Medical Confidence™ Service7: Receive faster access to care and treatment by appropriate physician specialists, a more accurate diagnosis, one-on-one support from a Registered Nurse and more.

- Waiver of Premium During Disability: Your premiums will be waived if you are disabled and being paid monthly benefits.

- Health Care Profession Rider: If you are a qualified health care professional, you will receive this rider at no additional cost. If you become HIV-impaired or hepatitis-impaired and, due to your impairment, you meet one of the conditions of the rider, you will be considered disabled9.

- Portable: You can keep your policy if you change jobs.

Who can apply?

Ages 18-60

Canadian citizens

Permanent residents/landed immigrants

What’s covered?5

The policy pays a disability benefit due to injury or illness if you:

- Have a reduced ability to work that results in a loss of earnings of 20% or more; and

- Are receiving the appropriate physician’s care (we may waive this requirement if we determine that continued care would not benefit you)

In addition, you are required to work in a reasonable occupation to the extent that you are able.

Customized return to work benefits provide financial benefits, as well as rehabilitation, retraining, work-site modifications and other services to assist you in returning to full-time work.

To ensure your benefits are coordinated with other sources of income received during disability, the policy includes an integration of benefits provision. If the sum of current earnings and other income or disability benefits exceeds 85% of your pre-disability income, then your payable benefits for disability will be reduced by that amount.

This is the number of days between the onset of a disability and the day you begin receiving benefits. You can choose from: 30, 60, 90, 120, 180, 365 and 730 days. (The two-year benefit period is not available with a 730-day elimination period.)

Choose from the following optional coverage (subject to eligibility)5:

- Family Compassionate Care Rider: The Family Compassionate Leave rider provides a monthly benefit to insureds whose spouses or children are diagnosed with a terminal illness. The benefit matches the basic indemnity on the disability policy of the insured, and can continue to the earlier of 12 months of the death of the insured’s family member. Premiums on the disability policy are waived while the benefit is being paid.

*Not available with Wage Loss Replacement Plans - Long-Term Care Conversion Option: From age 55 to 65, you can convert all or some of your coverage to long-term care insurance, without providing evidence of good health

- Additional Monthly Benefits: Adds more coverage to your base coverage.

- Future Income Option: To keep pace with your rising income, this allows you to purchase additional coverage on each policy anniversary date, up to age 55, without having to prove your health status.

- Cost of Living Benefit: While you are disabled, this benefit protects you against inflation, subject to limits.

- Retirement Protector Rider: Helps you maintain deposits to a retirement savings plan (RSP) while you are totally disabled.

Benefits are not paid for disabilities due to:

- An act or accident of war

- Normal pregnancy or childbirth (complications of pregnancy or childbirth are covered)

- Any injury sustained or illness which first manifests itself before your policy becomes effective or while your policy is not in force

In addition, the policy won’t pay a benefit for any period during which you are incarcerated.

About your premiums

Premiums for injury coverage cannot be changed unless we do so for an entire group of policyholders sharing similar characteristics

Step rate premiums (ages 18-35 only), which let you pay less while you’re getting your career off the ground (guaranteed to age 65)

Pay no premiums while you’re collecting benefits (after you have been disabled for 90 days).

- Guaranteed renewable to age 65 (policy can’t be changed or canceled without your consent)

- After age 65, while you are employed full-time in a gainful occupation up to age 75, you may continue the policy for 24 months; thereafter, the maximum benefit period is 12 months

Policy documents:

The information above is intended as a summary only.

For retirement planning

Disability insurance

Retirement Protector

Save for your retirement—even if a disability keeps you from earning. An ideal companion policy to our other disability plans, the Retirement Protector policy will make contributions to your retirement savings plan (RSP) if you experience a total disability.

Ideal if you

Are currently contributing to an RSP

Don’t have a company pension plan

Highlights

RSP contributions: If an injury or illness prevents you from working, the policy will continue making contributions to your RSP.6

Non-cancellable and guaranteed continuable: Policy cannot be cancelled without your consent, up until age 65.

Benefit period: Depending on your occupation, you can receive benefits for either 10 years or to age 65.

Portable: You can keep your policy if you change jobs.

- Rehabilitation: If you enter an approved vocational rehabilitation program, we will waive the requirement of total disability and help pay for the program, subject to the terms of your policy.

- Health Care Profession Rider: If you are a qualified health care professional, you will receive this rider at no additional cost. If you become HIV-impaired or hepatitis-impaired and, due to your impairment, you meet one of the conditions of the rider, you will be considered disabled.9

Who can apply?

Ages 18-55

Canadian citizens

Permanent residents/landed immigrants

What’s covered?5

- Total disability benefits between $300 and $1,500 per month13 are payable if, due to injury or illness, you are:

- Unable to perform the important duties of your regular occupation, and

- Not engaged in any other gainful occupation, and

- Receiving appropriate physician’s care and treatment

- Note: If you purchase the policy as a rider to one of our other disability insurance plans, you are protected in your regular occupation as defined by the policy to which the rider is attached. The benefit is paid for total disability only. If you purchased The Foundation Series™ policy with the Enhanced Definition of Disability Benefit rider, this enhanced definition will also apply to the Retirement Protector rider.

- Health Care Profession Rider: If you are a qualified health care professional, you will receive this rider at no additional cost. If you become HIV-impaired or hepatitis-impaired and, due to your impairment, you meet one of the conditions of the rider, you will be considered disabled.9

This is the number of days between the onset of a disability and the day you begin receiving benefits.

- If you purchase the Retirement Protector policy as a rider to another plan, the elimination period is the greater of 90 days or the elimination period of the policy to which the rider is attached.

- If you purchase the Retirement Protector policy by itself, the elimination period is 90 days.

Benefits are not paid for disabilities due to:

- Normal pregnancy or childbirth (complications of pregnancy or childbirth are covered)

- An act or accident of war

About your premiums

As long as you pay your premiums as required, we cannot cancel the policy without your consent, up until you turn 65

Pay no premiums while you’re collecting benefits

Policy documents:

The information above is intended as a summary only.

Term life insurance

A popular choice if you want affordable coverage until you meet a certain financial milestone, such as putting your kids through college or paying off your mortgage.

Term life insurance

Most popular

RBC Simplified Term Life Insurance

Get affordable protection for all your short-term needs with a path towards lifetime coverage.

Highlights

Learn more

Tools to get the most out of your coverage

Disability insurance calculator

Answer a couple questions and we’ll recommend the right amount of coverage.

Compare disability insurance plans

There’s a plan to suit your unique situation and needs—let’s help you find it.

Whatever your needs, we can help.

Protect your income with disability insurance—get an online quote or talk to a licensed

insurance advisor.

Need help now? Call 1-866-262-7924

Note: Online quote is for RBC Simplified® Disability Insurance only.

Frequently asked questions about disability insurance

-

General insurance

-

Applying for coverage

-

Eligibility

-

Coverage details

-

Premiums

Still have questions? Contact us.

General insurance

While the Canada Pension Plan (CPP) and Quebec Pension Plan (QPP) do include disability coverage, there are considerable limitations to the benefits provided by these plans:

- For 2026, the average monthly CPP disability benefit is $1,210.86 and the maximum monthly amount is $1,741.20. This amount is considerably less than what you could receive through one of our disability insurance plans. For example, through The Professional Series policy, some individuals can qualify for as much as $25,000 per month, depending on their occupation, pre-disability income and other factors.

- To qualify for the CPP disability benefit, you must sustain a severe and prolonged mental or physical disability and be unable to work at any occupation. With a disability insurance plan from RBC Insurance, you may be able to receive benefits under a less stringent definition of disability.

Learn more at: https://www.canada.ca/en/services/benefits/publicpensions/cpp-disability-benefit/benefit-amount.html.

This answer depends on your employer-sponsored disability plan, so examine it carefully and know what it covers. Typically, an employer-sponsored plan will end when your employment ends. One of the advantages of a disability insurance policy from RBC Insurance is that you can take it with you if you leave your job.

Here are some things to look at for your employer-sponsored plan:

- How much of your income will your employer-sponsored disability plan replace? Will you be caught short?

- Are you covered for illness as well as injury?

- Are you only covered for accidents on the job, or are you protected 24/7?

- Does your plan provide valuable return to work services?

- How does your plan define a disability?

Once you know the answers to these questions, you may find that you need additional coverage.

Your disability benefits should allow you and your family to continue to live comfortably, as though you were still able to work full-time. First, total up your monthly “fixed living expenses” such as food, housing, transportation, utilities and other miscellaneous expenses. Subtract from that amount any income you’ll receive from other sources during a disability—for example, from investments you may have, property you rent out and other disability insurance coverage. The amount by which your expenses exceed income during disability is the amount you need. Bear in mind, though, that any disability insurance plan will only replace a portion of your income.

Applying for coverage

To apply:

To apply for RBC Simplified® Disability Insurance, you can also:

- Get a quote and apply online for injury-only coverage

- Get a quote and then call 1-866-262-7924 to apply for injury and sickness coverage

Typically, yes. When purchasing disability insurance, medical questions and exams are usually required, the extent of which depends on your age and the amount of insurance you request when you apply.

If you apply for RBC Simplified® Disability Insurance, there are just a few basic pre-qualifying questions and no medical exam.

Eligibility

You may apply for disability insurance if you:

- Meet the age requirements of the policy:

- Age 18-60 for The Professional Series®, The Foundation Series™, The Bridge Series® and Quantum policies

- Age 18-64 for The Fundamental™ Series policy (illness coverage) and age 18-69 (injury coverage)

- Age 18-55 for RBC Simplified® Disability Insurance

- Age 18-55 for the Retirement Protector policy

- Are a Canadian citizen or permanent resident/landed immigrant

We encourage you to apply even if you aren’t sure you can qualify. If you are not eligible for a traditional disability plan, you may be eligible to apply for RBC Simplified® Disability Insurance, which only requires answers to a few basic pre-qualifying questions.

Yes, he or she may apply for coverage under his or her own policy, provided your partner meets the eligibility requirements of the policy.

Coverage details

Disability insurance isn’t a “one size fits all” purchase. Different people have unique circumstances, needs and budgets. That’s why we offer such a wide range of policies with a variety of options.

You must meet the plan requirements for eligibility, including having the policy in force and satisfying the elimination or waiting period.

Definitions of disability vary from plan to plan; your policy will contain complete information about eligibility, limitations and exclusions.

The elimination period is the number of days between the onset of a disability and the day you begin receiving benefits. Most of our plans offer you a choice of elimination periods ranging from 30 days to 730 days. RBC Simplified® Disability Insurance has a 60-day or 90-day elimination period to choose from.

Yes. Typically, benefits are not paid for disabilities due to5 (the following is a summary of exclusions only):

- An act or accident of war

- Normal pregnancy or childbirth (complications of pregnancy or childbirth are covered)

In addition, the policies won’t pay a benefit for any period during which you are incarcerated.

Yes, you can cancel your coverage at any time by contacting us.

Premiums

You will pay premiums through the term of your policy.

This answer depends on the policy. Some plans offer a choice of guaranteed level premiums for the life of the contract and step rate premiums (for age 35 and under), which allow you to pay less while you’re getting your business or career off the ground. With other policies, RBC Insurance does reserve the right to increase premiums. However, we cannot change your premiums unless we do so for an entire group of policyholders sharing similar characteristics.

A Waiver of Premium benefit is included in every one of our disability insurance plans at no extra cost. In most policies, this provision takes effect after 90 days of disability and any premiums you paid during the 90 days are refunded back to you.

Still have questions? Contact us.

Availability, details and limits of return to work assistance benefits vary by insurance plan. Return to work benefits are not available with RBC Simplified® Disability Insurance. Contact an RBC Insurance® advisor for complete details.

If you are self-employed, income means your share (proportionate to your ownership interest) of the income or loss of the business net of all business expenses except income taxes. If you are an incorporated business owner, you may also include any wages, salary, fees or commissions which the incorporated business paid to you as an employee of the business. Certain conditions must be met for benefits to be payable. Your policy will provide complete details.

Provided you satisfy the pre-qualifying questions. Part-time is considered to be a minimum 30-hour work week.

This information is intended as a summary only. Other limitations may apply depending on the policy. Your policy will contain complete details on terms and conditions, including benefits and exclusions.

Certain conditions must be met for benefits to be payable. Your policy will provide complete details..

Certain conditions apply

Some conversion restrictions apply.

We reserve the right to charge premiums in the future.

10-year option is for certain occupations only.

Injury-only coverage is available if you satisfy a few pre-qualifying questions. You may also complete a short supplemental application to apply for illness coverage.

Some restrictions apply.

Your benefit will be 20% of your monthly earned income, as long as it is not less than $300 and not more than $1,500.

Available on Professional Series, The Foundation Series, The Bridge Series and The Quantum Series

Life expectancy under 12 months.

“Child” means Your own natural offspring, Your lawfully adopted child, or Your stepchild of any age until the rider expires at the age of 65 of the insured.

If the insured makes a claim after the date of diagnosis (i.e. a month or two after), we will pay retroactively to the date of diagnosis.