Life Insurance

Build Your Budget: Simple Steps, Tips, and Tricks

Home

Extra Coverage and Tips

Tools & Resources

Get in Touch

Talk to a Licensed Insurance Advisor at 1-877-749-7224

Auto

Car Insurance by Region

Specialty

Tools & Resources

Get in Touch

Talk to a Licensed Insurance Advisor at 1-877-749-7224

Life

Tools & Resources

Get in Touch

Talk to a Licensed Insurance Advisor at 1-866-223-7113

Injury & Illness

Tools & Resources

Get in Touch

Talk to a Licensed Insurance Advisor at 1-866-223-7113

Travel

Tools & Resources

Travel Insurance by Trip Type

Get in Touch

Call 1-866-896-8172

Credit & Loans

Tools & Resources

Get in Touch

LoanProtector & HomeProtector 1-800-769-2523

BalanceProtector Max 1-800-769-2512

Insurance Basics

Life Events

Featured Articles

Get in Touch

Talk to a Licensed Insurance Advisor at 1-800-769-2568

By Author: Shannon Lee Miller Graphics: Shannon Lattin • Published July 9, 2020 • 4 Min Read

Two central aspects of budgeting are prioritization and the ability to be fluid. You prioritize how you spend your money so that it goes towards the things that are essential for your lifestyle and will help you achieve your goals. If your financial situation ever changes, fluidity is important so that you can re-budget and reprioritize based on your new reality. Findings from the 2019 Canadian Financial Capability Survey show that about half of Canadians (49 per cent) use a budget to manage their money.

Setting a budget can be beneficial, but creating one might not always feel compelling. It’s good to have a goal in mind when you create a budget so you’re more likely to stick to it.

Goals may include:

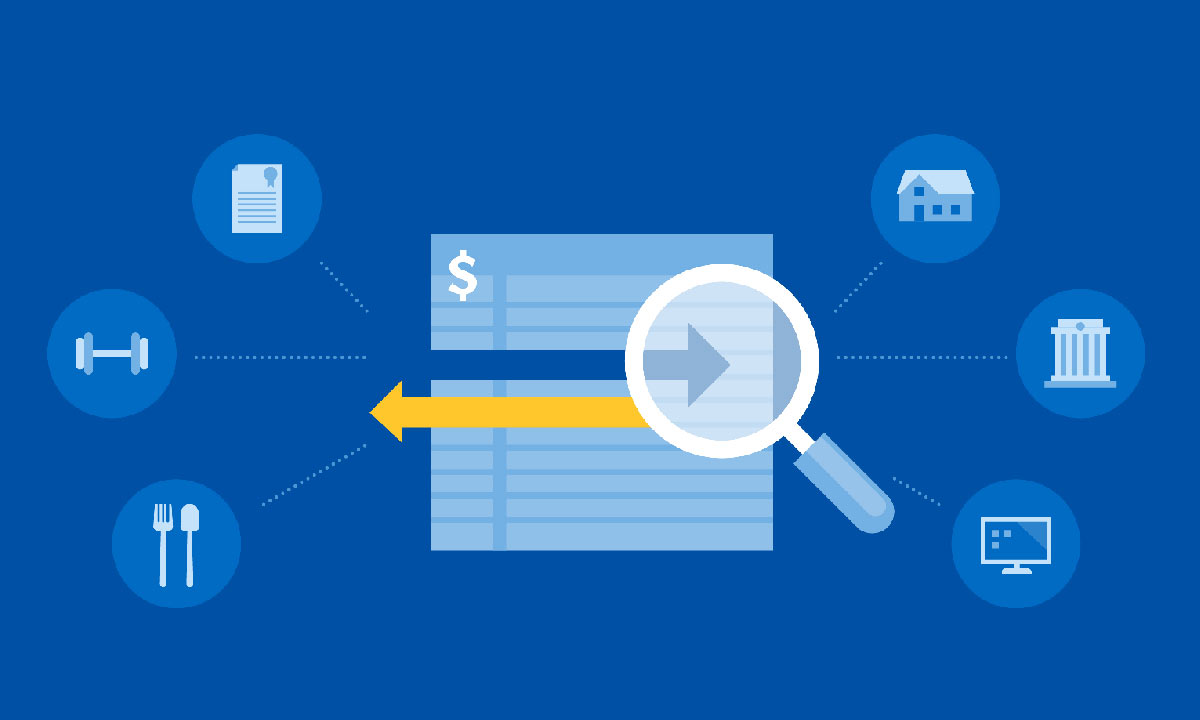

Calculate your monthly income and monthly expenses. In order to use more accurate numbers for this calculation, try to track everything you spend for one to two months. Remember to include things like your morning coffee, take out dinners and entertainment. This will give you a good idea of where your money goes. Tracking every single purchase might be difficult to do if this is new for you. See if your bank offers a service that tracks your spending, like the RBC NOMI app. Be extra mindful of the cash purchases you make and don’t forget to track them in a spreadsheet, a note in your phone or by using an app. There are apps available like Mint or Pocketguard, but do your research first to find one you’re comfortable using.

Once you have these results, compare what you make after taxes each month to what you spend.

If your expenditures are higher than your income, your first step is to reduce expenses where possible. This can be done in a number of ways — like cutting streaming services you don’t use often, curbing that excessive take out habit or something more significant like getting rid of a car.

Divide costs into fixed, flexible, and future.

A great way to divide these costs is by using the efficient 50-30-20 rule.

Set aside time each month to check-in. If you’re having trouble sticking to your budget, it might be time to try something new. You want your budget to be realistic and not the new mission impossible.

Find YOUR maintenance approach. Track spending with a spreadsheet, carry a set amount of cash instead of credit, or like 20 per cent of Canadians, try software or a mobile app to monitor money. Some helpful tools include Mint, Mvelopes, and Budget Planner by the FCAC. Whatever the approach, find a strategy that works for you.

Source:

Financial Consumer Agency of Canada. Canadians And Their Money: Key Findings from the 2019 Financial Capability Survey. 2019.

View Text Version of Illustration

50% Fixed costs aka “the essentials.”

This list may be different for everyone.

DID YOU KNOW? It’s recommended that your total housing costs be no more than 30-32% of your gross income.

30% Flexible costs aka “the non-essentials”

FACT: Budgeters are less likely than non-budgeters to spend beyond their monthly income (18 vs. 29%)

20% Future costs aka “the eventuals”

TIP: If you are paid on a bi-weekly basis and set aside $50 each paycheque, you can save $1,300 in one year, before any interest.

*Home and auto insurance products are distributed by RBC Insurance Agency Ltd. and underwritten by Aviva General Insurance Company. In Quebec, RBC Insurance Agency Ltd. Is registered as a damage insurance agency. As a result of government-run auto insurance plans, auto insurance is not available through RBC Insurance in Manitoba, Saskatchewan and British Columbia.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

Share This Article

Read This Next

9 Min Read

7 Min Read

9 Min Read

Whatever You Need, We Can Help

Speak with an RBC Insurance Advisor: 1-888-925-0946 or Have an Advisor Call Me

Want to meet? Find an Advisor or Store